See the upper left of the $100 bill? It says FEDERAL RESERVE NOTE. Similarly, the check shown above right is also a note (aka promise that the bank(s) can transfer $1000 upon receipt of the check.) When purchasing a car via a loan, that loan is a promissory note to pay the lender back over time.

In the context of real estate, the word note is short for Promissory Note, which is a legally binding agreement between borrower and lender (sometimes the seller is the lender) guaranteeing the borrower will reimburse the lender over an agreed timeframe with agreed monthly payments. Failure to reimburse results in late fees, possible loan modification, a cash for keys transaction, or if things get that far, foreclosure.

When you purchase a home, if you have enough cash on hand to purchase outright, no loan is needed. Still lots of paperwork, but no loan. Most of us are not that fortunate.

If, on the other hand, you don’t have sufficient cash, you will typically make arrangements with a lender. These arrangements will require credit check, tax returns, pay stubs, bank statements, 401K statements, and likely a few other things. What pops out at the end of this ordeal is an agreement between you (the borrower) and your lender that specifies the term of the loan, the interest rate, the down payment, and the monthly payments. Monthly payments will for sure include principle and interest, and perhaps tax and insurance.

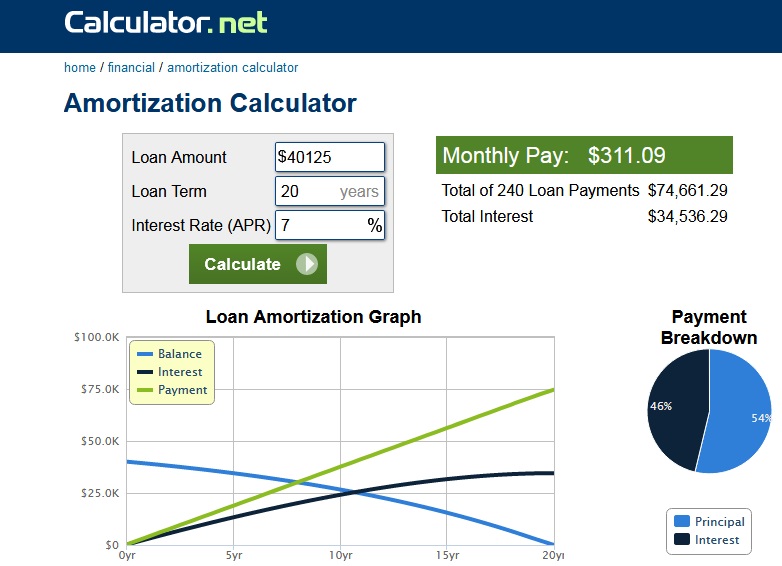

By law, lenders must provide borrowers with an amortization schedule. A graphical summary of the amortization is included below, using

https://www.calculator.net/amortization-calculator.html.

Note the difference between the light blue and the dark blue in the Payment Breakdown. By purchasing notes, we earn the interest. We’d love to share this with you by selling you a partial note.

This short video provides a brief synopsis on Note Investing.